Introduction

Financial services firms spend billions on compliance infrastructure, digital transformation, and strategic repositioning. Yet misconduct persists, employee disengagement climbs, and transformation programs stall. The reason is rarely the strategy — it's the culture.

Regulators have been direct about this. The FCA identified culture as "a key root cause of the major conduct failings" in financial services. The Financial Stability Board traced weaknesses in risk culture directly to the global financial crisis. After 2008, large financial firms paid more than $320 billion in aggregate misconduct-related fines — a number that reflects what cultural dysfunction actually costs at scale.

What doesn't work: values statements on walls, communications campaigns, and town halls about "doing the right thing." These change what leaders say, not what employees do. Real culture change requires identifying, measuring, and deliberately shaping the behaviors that define how an organization actually operates — consistently, at every level of the organization.

This guide covers how to assess your current culture, identify the specific behaviors driving dysfunction, and build a structured path toward lasting change.

Key Takeaways

- Culture is not what leaders declare — it's what behaviors get consistently reinforced and rewarded in practice.

- Most cultural assessments measure satisfaction; effective ones map the specific behaviors, reinforcers, and consequences driving how employees actually work.

- Applied Behavior Analysis (ABA) provides the most evidence-based framework for diagnosing and transforming culture that sticks.

- Leaders are the most powerful force shaping culture — their attention and reactions matter more than any stated values.

- Culture change in large financial institutions requires 18–36 months of deliberate, structured effort.

What Makes Financial Services Culture Uniquely Challenging

Financial services organizations are structurally designed for risk-aversion and hierarchical control — and those same features that make institutions stable create powerful resistance to behavioral change. When new values are announced, the old reinforcers keep working. Stability and cultural agility pull in opposite directions, and stability usually wins by default.

The Compliance-by-Fear Problem

Regulatory pressure has a specific and well-documented cultural side effect: it produces compliance-by-fear rather than genuine cultural alignment.

When employees follow rules primarily to avoid regulatory censure or personal consequences, behavior is surface-level and fragile. The moment oversight relaxes — or when a high-pressure sales target conflicts with a compliance requirement — the fear-based behavior breaks down. This is precisely what the BIS and New York Fed identified when they described environments where "rules may be followed to the letter, but not in spirit."

Genuine cultural alignment looks different. Employees understand why certain behaviors matter for customers, the institution, and the markets it serves. That understanding is reinforced positively — not just avoided negatively.

The compliance-culture gap is expensive on its own. But it's compounded by a second pressure that's harder to fix with policy.

The Competitive Urgency

McKinsey projects fintech revenues will grow at 15% annually through 2028 — more than three times the projected growth rate of traditional banking revenues. Fintechs compete partly on product, but mostly on how their people behave: faster decisions, higher tolerance for experimentation, and a willingness to prioritize the customer interaction over the internal approval chain. Legacy institutions struggle to replicate those behaviors when their reinforcement structures reward caution over initiative.

Culture transformation has moved off the HR agenda and onto the executive agenda. The question now is whether to lead the change deliberately — or react to it after market share has already shifted.

Why Culture Is the Real Driver of Performance in Financial Services

Defining Culture Through a Behavioral Lens

Abstract definitions of culture — "the way we do things around here," "our shared values" — are functionally useless for diagnosis or change. ADI's definition is more precise and more useful in practice: culture is the patterns of behavior strengthened or weakened by people or systems over time.

This definition matters because it shifts focus from aspiration to observation. If you want to understand a firm's real culture, don't read the values statement. Watch what behaviors get recognized, tolerated, and punished in practice. As ADI puts it: "the behaviors that you're getting now are the ones that are currently being reinforced."

The Cost of Getting It Wrong

The financial cost of cultural dysfunction in this sector is not theoretical:

- $320 billion+ in aggregate misconduct fines paid by large financial firms after 2008

- $100 billion+ in fines on the largest U.S. banks alone

- Demonstrably higher bank risk associated with poor organizational culture, per Bank of England research

- Wells Fargo's sales scandal — rooted in what its own independent board report called "the distortion of the Community Bank's sales culture and performance management system"

The Wells Fargo case is instructive. Approximately 5,300 employees were terminated for sales-practice violations between 2011 and 2016. The root cause wasn't individual ethics failures: it was a reinforcement system that rewarded sales volume regardless of how it was achieved.

Discretionary Effort: Why Culture Determines Performance Ceiling

ADI's concept of Discretionary Effort explains the performance gap between high-performing and fear-driven cultures. Discretionary Effort is the level of effort employees could give if they wanted to, above and beyond the minimum required. The key word is want to.

Positive reinforcement builds that motivation. Fear-based management produces "have to" compliance instead, and research consistently shows that compliance caps performance at whatever level avoids consequences — nothing more.

Organizations that earn Discretionary Effort consistently outperform those that don't. ADI's insurance sector client data illustrates this concretely:

- 1,500% rise in net production at a national healthcare insurance provider after implementing behavior-based performance management

- 50% decrease in customer complaints over the same period

- 20 years of sustained improvement — not a one-quarter spike

Culture as a Regulatory and Governance Issue

Culture is no longer solely an HR domain. OSFI now explicitly requires federally regulated financial institutions to integrate culture risk into enterprise-wide risk management. The FCA, Federal Reserve, and APRA have all identified culture as a supervisory concern and a root cause of systemic conduct failures.

For financial services leaders, that regulatory posture has a practical implication: culture assessment can no longer wait for a conduct failure to trigger it. It belongs on the risk agenda before problems emerge.

How to Conduct a Financial Services Cultural Assessment

Why Most Assessments Fall Short

Standard employee engagement surveys measure how people feel about their work. They don't reveal which behaviors are being reinforced, how leaders actually respond to mistakes, or whether ethical conduct is genuinely rewarded or only symbolically promoted.

A 2025 Journal of Management Control study confirms this directly: traditional quantitative tools and surveys fail to capture the complexity of risk culture. Effective assessments require triangulation through interviews, behavioral observation, document analysis, and qualitative evidence. One-time snapshots miss adaptation and resistance patterns that only longitudinal analysis reveals.

There's also a social desirability problem. The FCA has noted that when unethical behavior becomes normalized, surveys miss it entirely — and has recommended unobtrusive behavioral indicators (linguistic analysis of internal communications, external review data) to reduce that bias.

A Behavioral Assessment Approach

ADI's culture assessment methodology is built around this distinction: don't ask employees how they feel about values — identify the specific, observable behaviors that define high performance versus risk, and map the consequences currently driving those behaviors.

The process combines two elements:

- Culture Survey — gives employees a structured voice and captures perceptions of organizational strengths and improvement areas; designed to detect behavioral patterns, not sentiment

- Site Assessments — interviews, focus groups, and direct behavioral observation to provide the depth and clarity the survey alone can't deliver

Together, they reveal what the organization is actually reinforcing — not what it intends to reinforce.

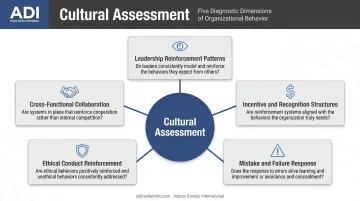

Key Dimensions to Examine

A thorough financial services cultural assessment should map:

- Leadership reinforcement patterns — which behaviors do senior leaders actively recognize, overlook, or subtly discourage through their day-to-day responses?

- Incentive and recognition structures — do compensation systems reward how results are achieved, or just that they are achieved?

- Mistake and failure response — how are errors and near-misses actually handled compared to what policy documents say?

- Ethical conduct reinforcement — is doing the right thing positively reinforced, or only punished when it goes wrong?

- Cross-functional collaboration — do structural incentives drive cooperation across units, or quietly reward siloed behavior?

Mapping Subcultures

Large financial institutions don't have one culture — they have many. A retail banking division, a trading floor, a compliance function, and a technology team can operate with distinct behavioral norms even within the same firm. Effective assessments segment findings by business unit, geography, and function so that interventions target the right behavioral patterns where they're actually needed.

A Behavioral Science Framework for Culture Transformation

The Foundational Principle

Culture cannot be changed by declaring new values. Culture changes when new behaviors become habitual because they are consistently and positively reinforced. That's not a management opinion — it's the fundamental finding of behavioral science, with a 1997 meta-analysis in the Academy of Management Journal documenting a 17% average increase in task performance from organizational behavior modification programs.

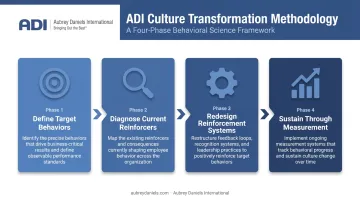

The Four-Phase Transformation Process

ADI's behavioral transformation methodology follows a defined sequence:

- Define target behaviors — what does the desired culture look like in specific, observable behavioral terms across roles and levels? Not "be customer-centric" but the precise behaviors that customer-centricity requires at each position.

- Diagnose current reinforcers — what consequences are maintaining the undesired behaviors right now? This is where most organizations have blind spots: they focus on what behaviors they want and skip diagnosing why the current behaviors are so persistent.

- Redesign reinforcement systems — restructure recognition, feedback, compensation, and leadership attention to make target behaviors more likely. This is the operating model work: changing not just what leaders say, but what they do when an employee exhibits the right behavior.

- Sustain through measurement — track behavioral adoption continuously and adjust reinforcers to maintain progress. ADI's Behavioral Roadmapping defines critical behaviors at each organizational level — giving leaders a measurable tracking framework instead of relying on periodic surveys alone.

Shifting from Fear to Positive Reinforcement

In financial services, fear is the default management lever. Fear of regulators, fear of performance consequences, fear of reputational damage. Fear produces compliance. It does not produce Discretionary Effort, innovation, or the ethical judgment needed in complex situations.

ADI's Precision Leadership® approach directly addresses this. The methodology trains leaders to provide consequences that build rather than constrain performance — moving organizations from a "shame-and-blame" dynamic to one of coaching, recognition, and positive accountability. Firms that make this shift see behavioral change take hold at the frontline level, not just in values statements on a wall.

Wells Fargo's response is a useful case study in what not to do: eliminating sales goals in 2016 removed a negative incentive but did not create positive reinforcement for the desired service behaviors. Removing fear alone doesn't build a positive culture.

Building Internal Capability

Lasting transformation requires building internal leaders who can sustain behavior-based coaching and reinforcement long after an external engagement concludes. ADI's Trainer Certification and Coach Certification programs are specifically designed for this: equipping internal practitioners to facilitate behavioral leadership training and provide the ongoing follow-up coaching that turns short-term behavioral shifts into permanent habits.

Organizations that rely entirely on external intervention for culture change never develop the internal muscle to sustain it. Internalized capability — not ongoing dependency on outside consultants — is the measure of a successful engagement.

The Leadership Imperative: How Executives Shape Culture Daily

Senior leaders are the most powerful reinforcement environment in any financial services organization. What leaders pay attention to, what they recognize, what they question, what they ignore, and what they react to emotionally — all of it sends constant behavioral signals to everyone watching.

The gap between stated culture and actual culture is almost always a leadership behavior gap. A leader who says "we value innovation" but visibly withdraws support from a failed initiative teaches everyone in the room that innovation is only valued when it succeeds. That lesson spreads faster than any memo about psychological safety.

What Culture-Building Leaders Do Differently

Research from McKinsey found that only 43% of employees report a positive team climate — and positive team climate is the strongest driver of psychological safety, which in turn is the foundation of speaking up, ethical challenge, and adaptive performance.

Culture-building leaders in financial services demonstrate specific, distinguishable behaviors:

- Specific, immediate positive reinforcement for target behaviors — not generic praise, but recognition tied to the precise behavior exhibited

- Personal behavioral modeling of the culture they're trying to build, with visible consistency between stated values and daily decisions

- Tolerance for productive failure in innovation contexts, distinguishing between errors of judgment and errors of competence

- Transparent communication connecting behavioral expectations to business outcomes, not just regulatory requirements

Developing the Next Generation

As the memory of the 2008 crisis fades, the next generation of financial services leaders needs deliberate behavioral development, not just technical competence. Deloitte's 2026 global survey found that only 6% of Gen Z and millennial employees cite achieving a leadership position as their primary career goal, while stability, skills, and well-being dominate their priorities.

Instilling ethical judgment requires more than classroom instruction about values. Effective development relies on:

- Experiential learning that puts leaders in realistic, high-stakes situations

- Scenario-based practice that builds judgment through repetition

- Mentorship that reinforces both ethical and performance behaviors in real time

Why Culture Transformation Efforts Fail — and How to Avoid It

McKinsey data puts large-scale transformation failure at approximately 70%. In financial services, several specific failure modes are well-documented.

The Four Most Common Failure Modes

| Failure Mode | What It Looks Like | Counter-Strategy |

|---|---|---|

| Communications campaign approach | New values, town halls, posters — no behavioral change | Diagnose reinforcement systems first; define target behaviors specifically |

| Skipping reinforcement diagnosis | Launching change without knowing why current behaviors persist | Use behavioral assessment to map what's maintaining the status quo |

| Fear as the only change lever | Relying on regulatory pressure to drive compliance | Build positive reinforcement structures alongside consequence management |

| Senior leader accountability gap | Leaders sponsor change but don't model or reinforce it | Make leader behavioral practices explicit, measurable, and accountable |

These failure modes aren't theoretical. The Wells Fargo and CBA Prudential Inquiry cases share a common thread: reinforcement systems — sales goals, performance management, promotion criteria — kept rewarding the wrong behaviors long after leadership announced cultural change. The stated culture diverged from the operational culture because the operating model was never redesigned.

Why Transformation Requires Continuity

The New York Fed stated plainly: culture reform in banking is a long journey, and no single action by a regulator or bank can complete it. The FCA echoes this — there is no organizational "quick fix."

Culture degrades when reinforcement structures aren't maintained. Initial transformation momentum is not self-sustaining. Organizations that achieve lasting change build ongoing measurement cycles, manager reinforcement routines, and periodic reassessment into the operating model — not just the transformation launch plan.

Sustainment requires structure, not good intentions. ADI's approach builds this into the engagement from the start:

- Follow-up coaching embedded as a core deliverable, not an optional add-on

- Behavioral roadmaps with ongoing measurement benchmarks

- Positive accountability systems that keep new behaviors reinforced as they become habitual

Frequently Asked Questions

What is an example of a cultural transformation in financial services?

USAA is one of the most documented examples, ranking highest in the 2024 J.D. Power Individual Annuity Study with a customer satisfaction score of 780. Its culture was built on mission clarity and consistent reinforcement of member-first behaviors. What defines successful transformations in this sector: leadership-modeled behavioral change backed by structural redesign, not messaging alone.

What is the financial services transformation process?

The core phases of transformation include:

- Assess current cultural behaviors and the reinforcers maintaining them

- Define target behaviors aligned to business strategy

- Redesign reinforcement systems: recognition, compensation, performance management

- Build manager capability through certification and coaching

- Measure behavioral adoption on an ongoing basis

ADI applies this framework across financial services organizations of all sizes and subsectors.

How do you assess financial services culture?

Go beyond engagement surveys. Identify which specific behaviors are being reinforced, rewarded, and tolerated in practice — including how leadership attention, promotion decisions, and incident responses signal what the organization truly values. Combine culture surveys with site assessments, behavioral observation, and document analysis for a complete picture.

Why do culture change initiatives fail in financial services?

Most initiatives focus on changing stated values or improving communications rather than diagnosing and redesigning the reinforcement structures — incentives, recognition, performance management — that maintain current behaviors. The underlying behavioral drivers of culture remain unchanged, so the old behaviors persist despite the new messaging.

What are the top three trends in financial services affecting culture?

Three trends are reshaping culture priorities in financial services:

- AI and digital transformation: McKinsey reports almost all companies are investing in AI, yet only 1% believe they've reached maturity — creating urgent demand for adaptive, learning-oriented cultures

- Regulatory scrutiny: Culture has become a governance and risk management priority alongside HR and compliance

- Workforce expectations: Employees increasingly expect psychological safety and purpose-driven environments, making positive reinforcement cultures a competitive necessity

How long does cultural transformation take in financial services?

Meaningful behavioral change in large financial services organizations typically requires 18–36 months of sustained effort. Early behavioral signals can be measurable within 6–12 months when reinforcement systems are effectively redesigned and leaders are actively modeling target behaviors. CBA's response to the APRA Prudential Inquiry — accepting enforceable undertakings in 2018 and meeting those obligations by 2022 — illustrates a realistic multi-year transformation arc.